Branch Closure Attrition Research

Reducing attrition risk due to branch closure through qual/quant data analysis

Client

Capital One

Role

Lead Researcher

Industry

Finance

Focus

Research and Strategy

The Challenge

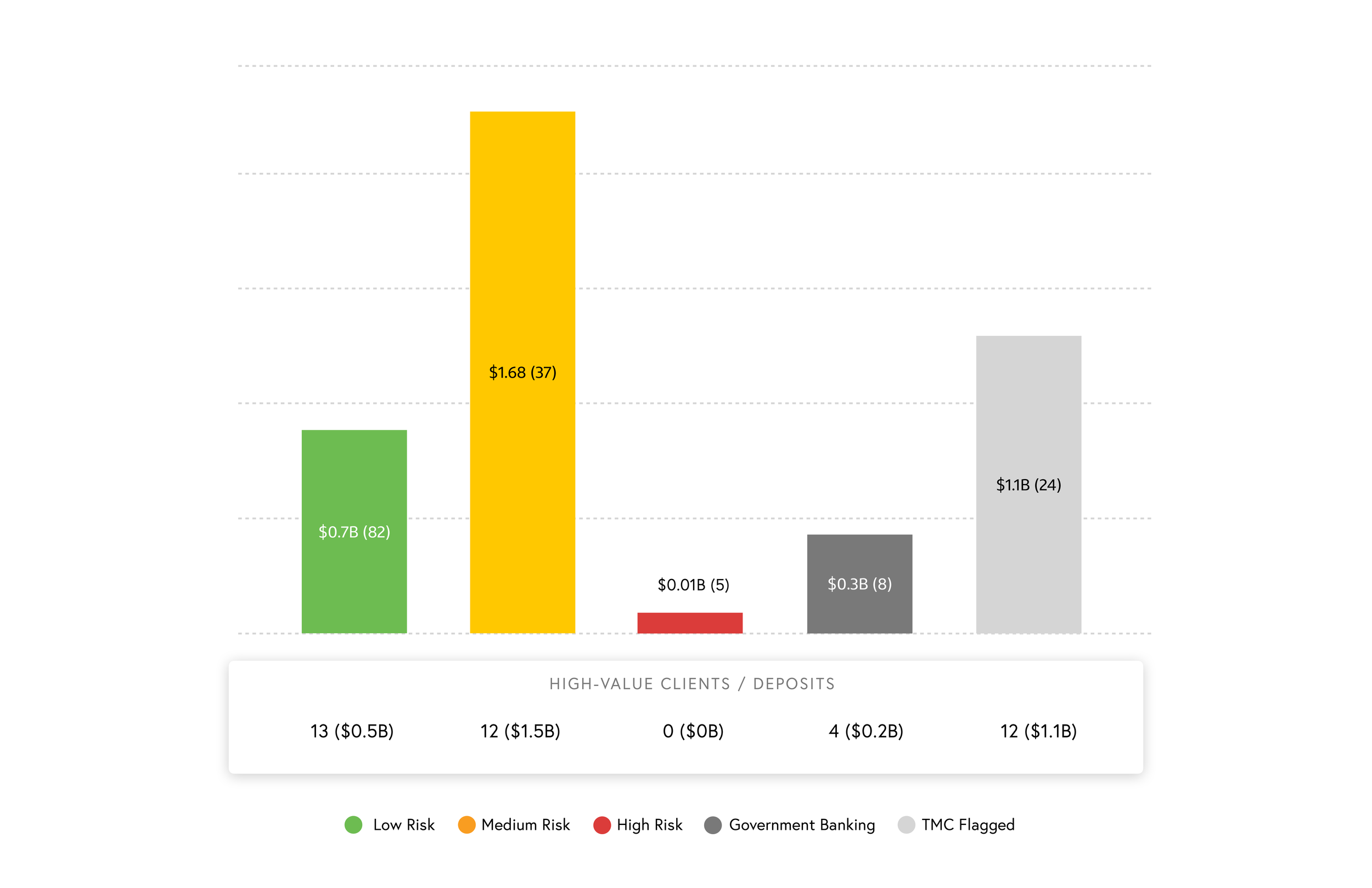

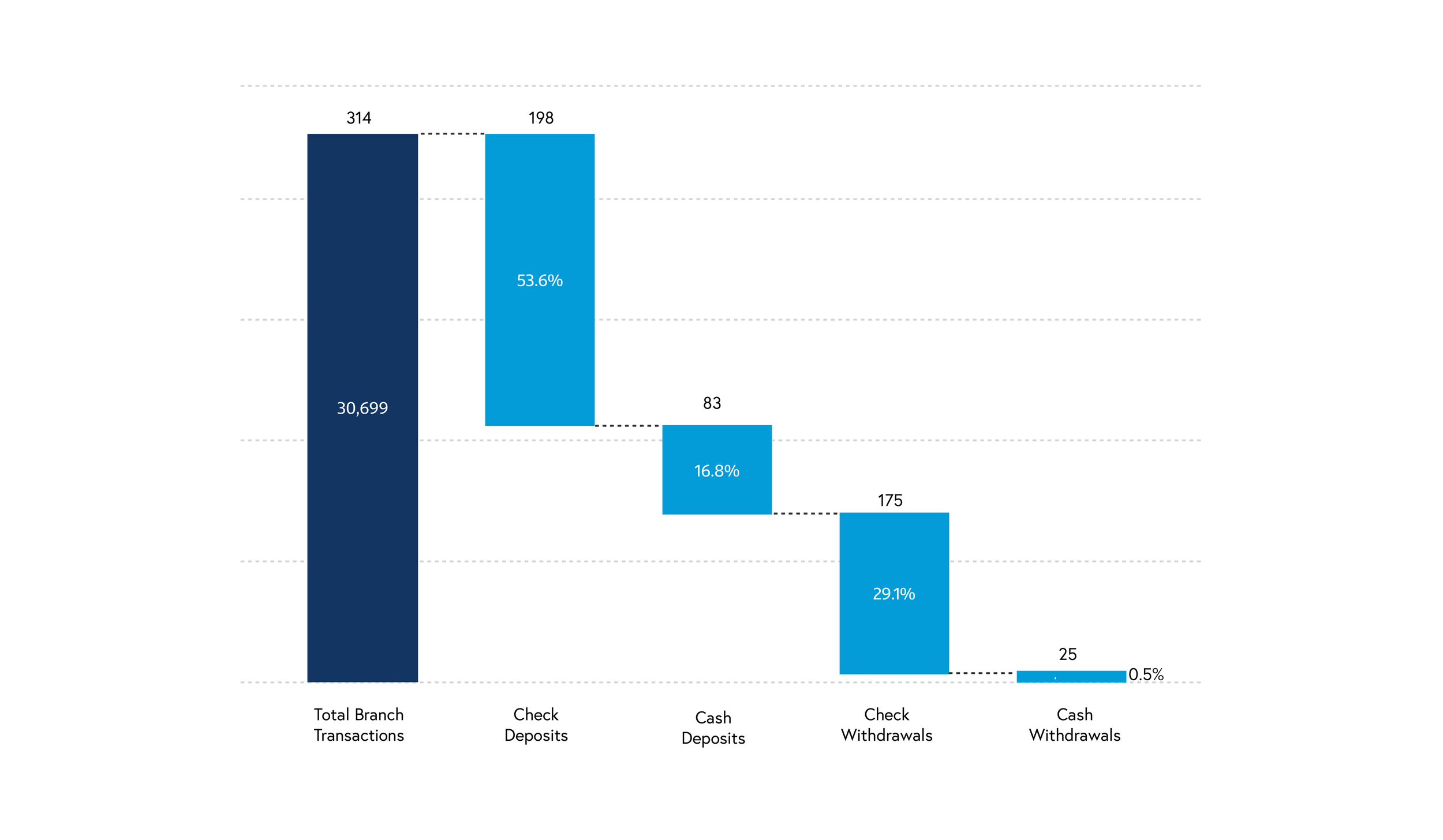

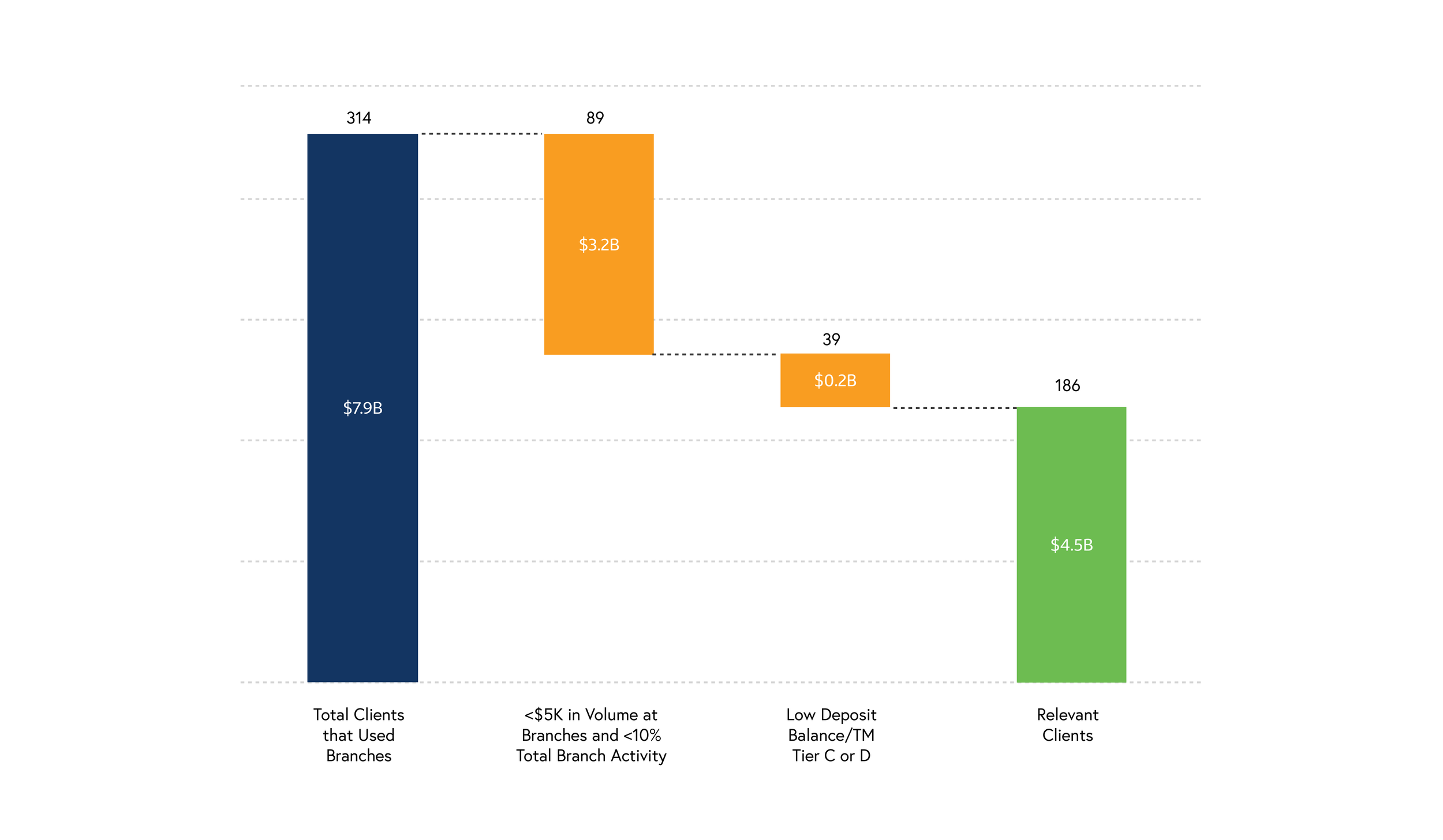

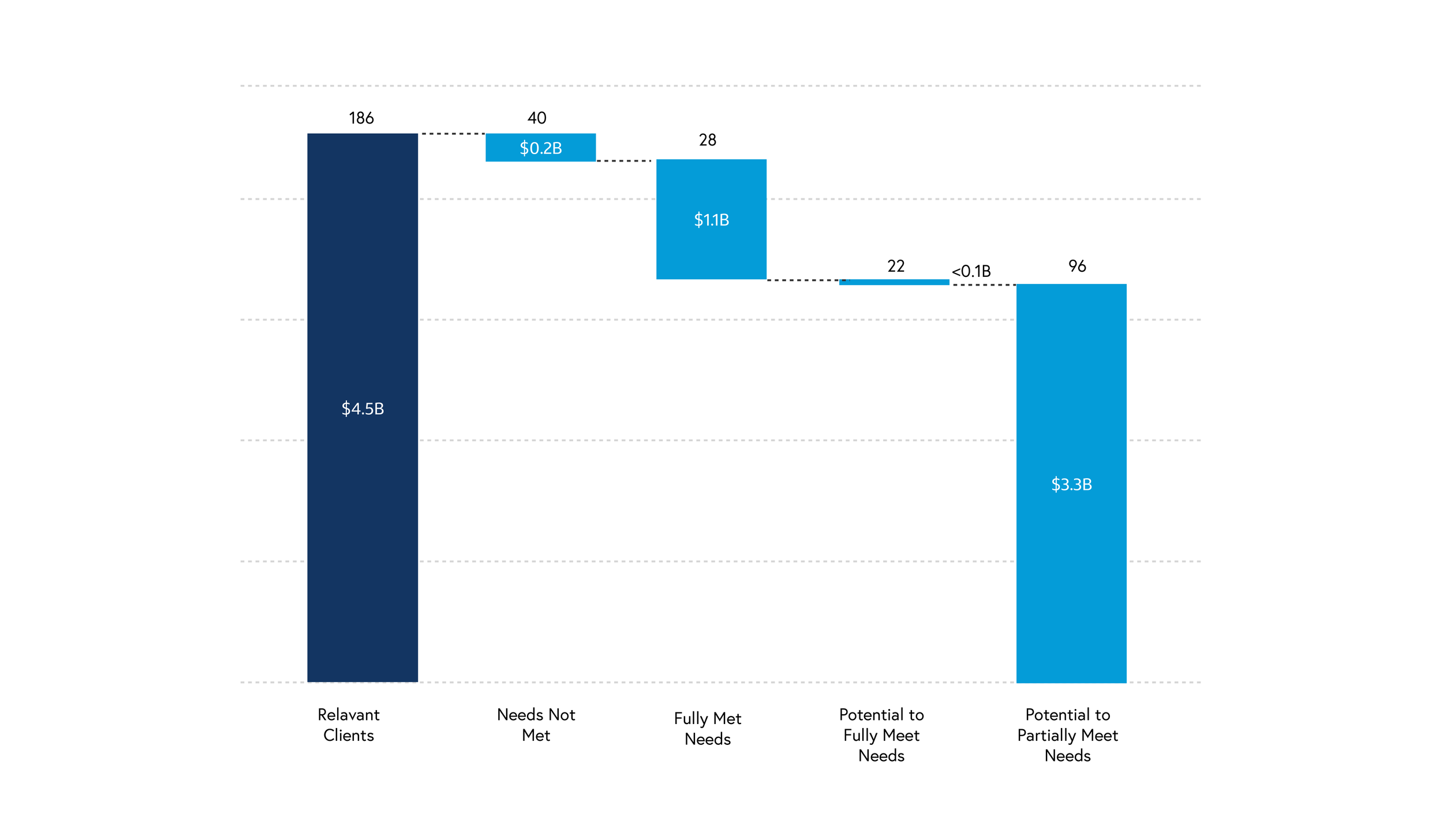

As part of Capital One’s goal of becoming a digital-first bank for both retail and Commercial clients, a series of branch closures were planned in specific region by 2024. This region represented $7.9 billion in deposits balances from 314 clients, and these clients are currently displaying some level of branch activity. The team was tasked to identify branch usage needs and client behaviors to incentivize use of existing branchless products and minimize attrition for high-value relationships.

Data Analysis

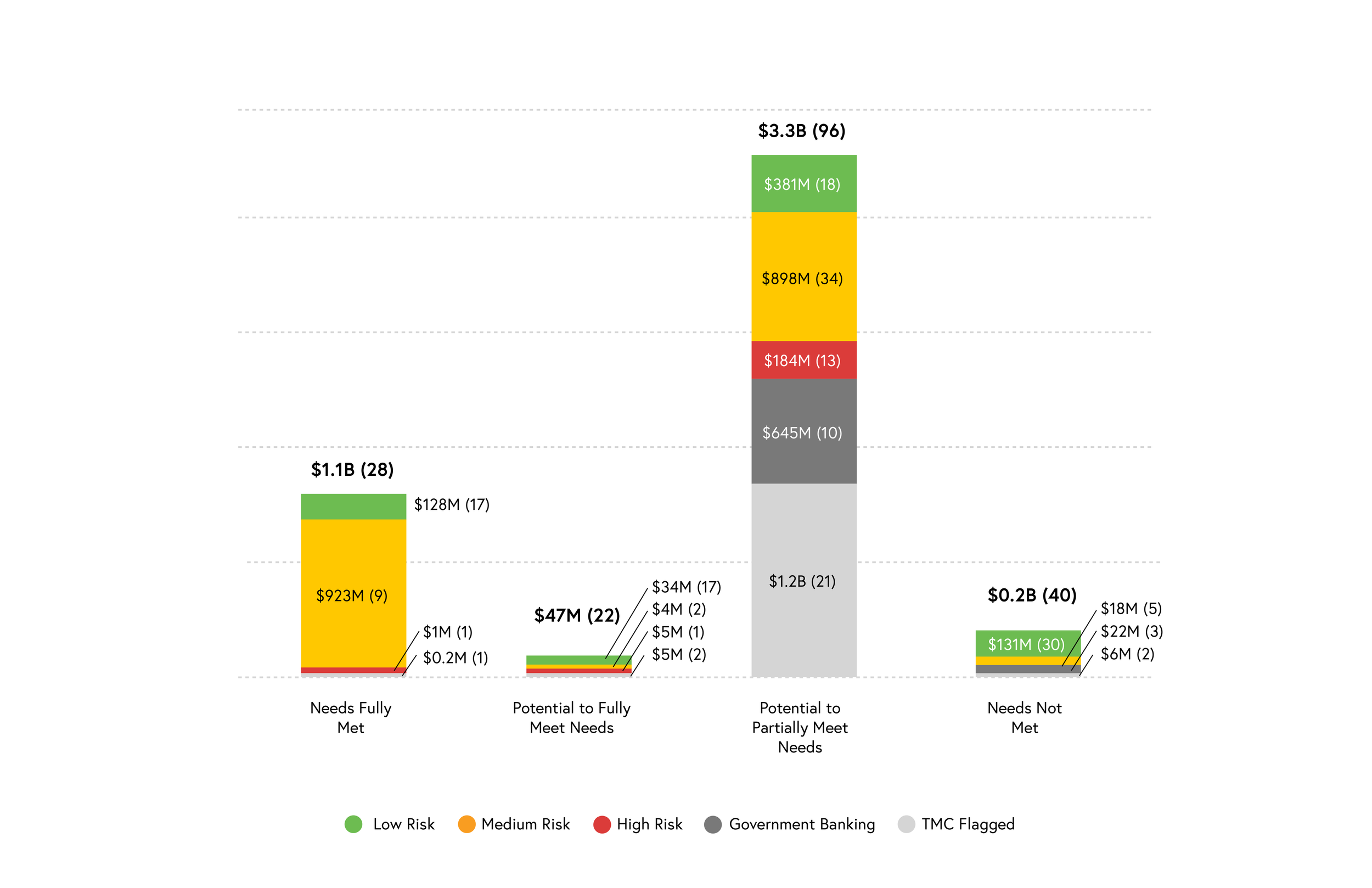

The Marketing & Analytics team analyzed over 30,000 branch transactions, including check handling and cash activity, across 300+ clients. Low-relevance data was filtered out by excluding clients with transactions under $5K or minimal branch reliance. The remaining clients were segmented by product coverage: unmet needs, fully met needs, and partial coverage. This segmentation provided an initial view of potential risk tied to gaps in branchless solutions.

Research

To validate and deepen the analysis, I partnered with branch associates and Treasury Management Consultants supporting key clients. This qualitative research revealed gaps in how data alone represented behavior. For example, check withdrawals often reflected payroll or vendor payments rather than preference for branch use. I synthesized findings into four archetypes, defined by reliance on cash operations and frequency of branch interactions.

Insight #1

A branch exit means a community exit, which has an impact on overall relationships, specifically in RCB.

Insight #2

State regulatory requirements dictate branch presence and/or payment types for some segments.

Insight #3

Branch dependency is higher when cash is germane to a client’s business model, and volume are low.

Insight #4

In some segments, cashier checks are required by the payee. This need is on-demand and time-sensitive.

Insight #5

Product performance issues impact our clients confidence in adopting branchless routines without a back-up.

Insight #6

Branch usage extends to clients’ employees and vendors. Caring for them will help us deliver holistic solutions.

Insight #7

TMCs have been offering alternative services to support branchless needs (but often lack visibility.)

Insight #8

Petty cash accounts or cash concentration can help large clients, but add complexity for smaller ones.

The Budgeted

High Branch Visits

Cash Is Germane

These clients have low transaction volumes and frequently use branches for deposits and change orders. Their volumes don’t justify adoption of branchless products and they’re reluctant to change daily operations to adapt (i.e. cash concentration). Oftentimes, branch proximity is what led them to bank with us in the first place.

The Transactor

High Branch Visits

Cash Is Ancillary

These clients need branches to make transactions and meet regulatory requirements from payees, state, county or city. Our product gaps (i.e. quick cashier checks provisioning) lead them to find suboptimal workarounds. Some need improved or new product features, for others, branch presence is a requirement.

The Go-Getter

Low Branch Visits

Cash Is Germane

These clients are typically high-ticket retailers or local B2B businesses with multiple locations. They use Vault, but proximity leads them into branches out of convenience, for deposits or emergency change orders. They are open to alternative solutions, like cash concentration or money orders, with no significant impact on daily operations.

The Improviser

Low Branch Visits

Cash Is Ancillary

These clients usually have higher volumes and are well cross-sold for their transaction needs. They only visit branches in exceptional cases, such as product malfunctions, transition periods (i.e. new locations) or for stakeholder needs, such as payroll and vendors. They’re open to adopt temporary solutions to avoid branch usage.

Use Cases

Working with the analytics team, I identified 12 use cases mapped across the four archetypes, combining transaction volume, visit frequency, and product adoption. Each use case was assigned a risk level: low, medium, or high, based on dependency on branch services and cross-sell potential. These were translated into data rules, enabling scalable identification of clients by behavior-driven attrition risk.

The Budgeted

Use Case #1

Cash withdrawal, cash deposit and check deposit volume is greater than the 25th pctl Vault volume.

Use Case #2

Cash withdrawal, cash deposit and check deposit volume is lower than the 25th pctl Vault volume.

The Go-Getter

Use Case #3

Visited a branch 6-12 months throughout the year for cash transactions or check deposits, using Vault.

Use Case #4

Visited a branch 6-12 months throughout the year for cash transactions or check deposits, using Vault.

The Improviser

Use Case #5

Visited a branch less than 6 unique months throughout the year to deposit or withdraw checks.

Use Case #6

Visited a branch 6-11 unique months throughout the year, not using Remote Deposit Check.

Use Case #7

Visited a branch 6-11 unique months throughout the year, using Remote Deposit Check.

Use Case #8

Visited a branch 6-11 unique months throughout the year to withdraw checks.

The Transactor

Use Case #9

Visited a branch every single month to deposit checks, not using Remote Deposit Check.

Use Case #10

Visited a branch every single month to deposit checks, using Remote Deposit Check.

Use Case #11

Visited a branch every single month to withdraw checks, with an avg. volume lower than $10k.

Use Case #12

Visited a branch every single month to withdraw checks, with an avg. volume higher than $10k.

Final Attrition Risk

By applying these data rules, I mapped each client to an archetype, primary use case, and corresponding risk level. Comparing this behavior-based model with the initial product-based analysis refined the results, isolating 41 high-value clients at elevated risk of attrition. These insights informed targeted cross-selling strategies, while the analytics team assessed when subsidizing solutions would be justified from a profitability standpoint.